Understanding tax terminology can feel overwhelming, especially when dealing with international rules and cross-border income. One of the most commonly used terms in U.S. tax law is “Non Resident Alien.”

This classification is used to describe individuals who are not U.S. citizens and do not meet the requirements to be treated as tax residents. It plays a key role in determining how much tax a person must pay and what forms they need to file.

For students, workers, freelancers, and investors earning income from the United States, knowing whether you fall under this category is very important. It directly affects how your income is taxed and what benefits or limitations apply to you under U.S. tax regulations managed by the Internal Revenue Service.

In this guide, we will break down the meaning of Non Resident Alien, how the status is determined, and what tax rules apply in a clear and simple way so you can fully understand your situation without confusion.

What is a Non Resident Alien? (Definition)

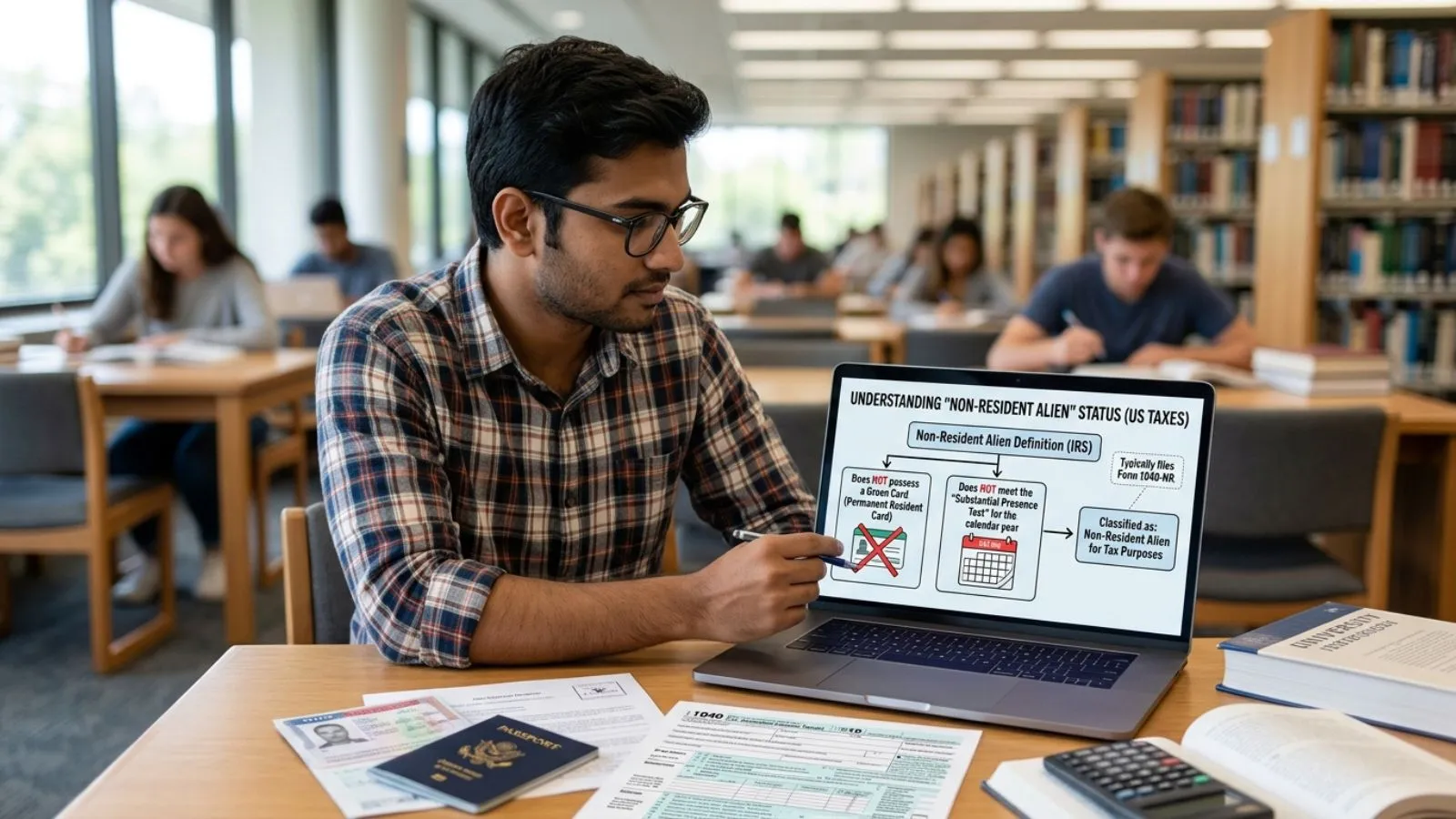

A Non Resident Alien (NRA) is a term used in U.S. tax law to describe a person who is not a U.S. citizen and does not meet the requirements to be treated as a tax resident of the United States. In simple words, it refers to individuals who either live outside the U.S. or stay in the country temporarily and do not pass specific residency tests set by tax authorities.

According to the rules established by the Internal Revenue Service, a person’s tax status is not only based on nationality but also on how long they stay in the United States and whether they meet certain legal conditions. This means someone can physically live in the U.S. but still be classified as a Non Resident Alien for tax purposes if they do not satisfy residency requirements.

A Non Resident Alien is typically taxed only on income earned from U.S. sources, such as wages from a job in the United States, income from U.S. businesses, or certain investments. They are not taxed on worldwide income like U.S. citizens or resident aliens.

It is also important to understand that “Non Resident Alien” is a tax classification, not an immigration status. This is a common point of confusion. Immigration status is controlled by visa or green card rules, while tax status is determined by specific IRS tests.

In short, a Non Resident Alien is anyone who is not considered a U.S. tax resident under IRS guidelines and is subject to special tax rules based on their U.S.-connected income.

Who Qualifies as a Non Resident Alien?

Not everyone who is living outside the United States automatically becomes a Non Resident Alien for tax purposes. The classification depends on specific rules set by the U.S. tax system. In general, a person qualifies as a Non Resident Alien (NRA) if they are not a U.S. citizen and do not meet the conditions required to be treated as a resident for tax purposes.

The first key requirement is nationality. If you are not a U.S. citizen, you may fall into the Non Resident Alien category. However, citizenship alone is not the final factor. The second and more important factor is whether you meet the residency tests defined by the Internal Revenue Service.

To be considered a resident for tax purposes, individuals must either pass the Green Card Test or the Substantial Presence Test. If a person does not meet either of these tests, they are generally classified as a Non Resident Alien. This applies even if they spend some time in the United States during the year.

Typically, Non Resident Aliens include international students, temporary workers, foreign investors, and individuals who earn income from U.S. sources but do not live in the country permanently. For example, someone working remotely from another country for a U.S. company may still be treated as an NRA depending on their physical presence and visa status.

It is important to understand that this classification is based on tax rules, not immigration rules. Therefore, a person’s visa type, length of stay, and physical presence all play a role in determining their tax status.

Tests Used to Determine Non Resident Alien Status

The classification of a Non Resident Alien (NRA) is not random; it is determined through specific legal tests used in U.S. tax law. These tests help decide whether an individual should be treated as a tax resident or a non resident for a given year. The two primary tests are the Green Card Test and the Substantial Presence Test, both established under rules enforced by the Internal Revenue Service.

1. Green Card Test

The Green Card Test is straightforward. If you are a lawful permanent resident of the United States at any time during the year, you automatically qualify as a resident alien for tax purposes. This means you are not considered a Non Resident Alien. Holding a green card is strong proof of tax residency, regardless of how many days you physically stay in the U.S.

2. Substantial Presence Test

This test is based on the number of days you are physically present in the United States. It uses a weighted formula that considers your stay over a three-year period. Generally, if you are present in the U.S. for at least 183 days in the current year (based on calculation rules), you may be classified as a tax resident instead of a Non Resident Alien.

3. Final Determination

If an individual does not meet either the Green Card Test or the Substantial Presence Test, they are classified as a Non Resident Alien. In some cases, special exceptions or tie-breaker rules may apply, but the general rule is simple: failing both tests results in NRA status.

Income Types Taxed for Non Resident Aliens

For Non Resident Aliens (NRAs), taxation in the United States is not based on global income but only on specific types of income connected to the U.S. This system is designed to ensure that only income earned from U.S. economic activity is subject to tax rules enforced by the Internal Revenue Service.

1. U.S.-Sourced Income

The most important category is U.S.-sourced income. This includes wages earned from jobs in the United States, payments for services performed in the U.S., business income generated within the country, and income from U.S. rental properties. If the income originates from within the U.S., it is generally taxable for NRAs.

2. FDAP Income (Fixed, Determinable, Annual, or Periodic Income)

Another major category is FDAP income. This includes passive income such as dividends from U.S. companies, interest from U.S. bank accounts, royalties, and certain pension payments. FDAP income is usually taxed through a withholding system, where a fixed percentage is deducted before payment is made.

3. Effectively Connected Income (ECI)

ECI refers to income that is directly linked to a trade or business conducted in the United States. This type of income is taxed more like a resident’s income and may allow deductions for related expenses. It often applies to NRAs who actively operate businesses in the U.S.

4. Withholding Rules

In many cases, taxes are withheld at the source before NRAs receive their income. The withholding rate depends on the type of income and any applicable tax treaties.

Best Tax Rates in Filing Requirements on Non Resident Aliens

Non Resident Aliens (NRAs) are subject to a unique tax system in the United States, where both tax rates and filing rules differ from those applied to citizens and resident aliens. The U.S. tax authority, the Internal Revenue Service, requires NRAs to report only their U.S.-sourced income, but the way this income is taxed depends on its type.

In general, wages and business income that are considered Effectively Connected Income (ECI) are taxed using the same progressive tax brackets as U.S. residents. This means the tax rate increases as income rises. However, NRAs are usually not eligible for the same standard deductions and tax credits unless a tax treaty allows it.

When it comes to filing requirements, most NRAs who earn U.S.-sourced income must file Form 1040-NR, which is specifically designed for non resident taxpayers. This form is used to report income, claim treaty benefits, and calculate the final tax liability.

1. Key Tax Benefits

One of the biggest advantages for NRAs is that they are only taxed on U.S.-sourced income, not global earnings. This can significantly reduce overall tax liability, especially for individuals who earn income in multiple countries. In addition, certain tax treaties between the U.S. and other countries may reduce withholding tax rates or even exempt specific types of income from taxation. These treaties help avoid double taxation and provide relief for eligible individuals.

2. Limited Deductions and Credits

Unlike resident taxpayers, NRAs generally cannot claim the standard deduction on their tax returns. Most personal tax credits, such as education credits or child tax credits, are also not available unless specifically allowed under a tax treaty. This limitation can increase the overall tax burden for some individuals.

3. Treaty-Based Exceptions

Some NRAs may qualify for additional benefits depending on their country of residence. Tax treaties may allow reduced tax rates on income like scholarships, pensions, or employment earnings. However, these benefits must be formally claimed when filing taxes.

4. Compliance Importance

Understanding these benefits and limitations is essential to ensure accurate tax filing and avoid overpaying taxes. Proper knowledge also helps NRAs take advantage of any available treaty provisions legally and effectively.

Non Resident Alien vs Resident Alien

Understanding the difference between a Non Resident Alien (NRA) and a Resident Alien is essential because it directly affects how taxes are calculated and what income is reported. These classifications are part of the U.S. tax system regulated by the Internal Revenue Service, and they are based on specific residency tests rather than nationality alone.

A Resident Alien is someone who either holds a U.S. green card or meets the Substantial Presence Test. Resident aliens are taxed similarly to U.S. citizens, which means they must report worldwide income—income earned both inside and outside the United States. They are also eligible for most tax deductions and credits.

In contrast, a Non Resident Alien does not meet these requirements. NRAs are taxed only on their U.S.-sourced income, which includes wages earned in the U.S., business income, and certain investments. They are generally not eligible for standard deductions or many tax credits unless a tax treaty provides special benefits.

Key Differences Summary

- Tax Scope: Residents pay tax on global income; NRAs only on U.S. income

- Eligibility: Residents meet Green Card or Substantial Presence Test; NRAs do not

- Tax Forms: Residents file Form 1040; NRAs file Form 1040-NR

- Benefits: Residents get full deductions; NRAs have limited benefits

Practical Impact

This distinction can significantly affect how much tax a person owes and what reporting obligations they must follow. For individuals moving between countries or working temporarily in the U.S., understanding this difference is critical to avoid filing errors and ensure compliance with U.S. tax laws.

Common Scenarios Explained for Non Resident Aliens

To fully understand Non Resident Alien (NRA) status, it helps to look at real-life situations where this classification applies. These examples show how different individuals may fall under NRA rules depending on their stay, income source, and tax residency status under guidelines set by the Internal Revenue Service.

1. International Students in the U.S.

A student from another country studying in the United States on an F1 or J1 visa is often considered a Non Resident Alien for tax purposes, especially in their first few years. Even if they earn part-time income on campus, they are generally taxed only on U.S.-sourced earnings and may be eligible for limited exemptions depending on their visa rules.

2. Remote Workers Outside the U.S.

A freelancer living in Pakistan, India, or another country who provides services to U.S.-based clients may also be classified as an NRA. Even though they are earning from the U.S., they are typically taxed only on that income and not on their global earnings.

3. Short-Term Business Visitors

Individuals who visit the U.S. temporarily for meetings, conferences, or short-term work assignments may still remain Non Resident Aliens if they do not meet residency tests. Their income, if any, is taxed based on U.S. source rules.

4. Mixed-Status Year

Some individuals may start the year as NRAs and later become resident aliens if they stay longer in the U.S. This creates a “dual-status” situation where different tax rules apply within the same year.

Common Mistakes to Avoid as a Non Resident Alien

Many individuals classified as Non Resident Aliens (NRAs) make avoidable mistakes when dealing with U.S. tax rules. These errors can lead to overpaying taxes, filing incorrect forms, or even facing penalties. The U.S. tax system managed by the Internal Revenue Service is strict about proper classification and accurate reporting, so understanding these mistakes is very important.

1. Confusing Immigration Status with Tax Status

One of the most common mistakes is assuming that visa status automatically determines tax status. For example, having a student or work visa does not always define whether you are a Non Resident Alien or resident for tax purposes. Tax status is based on IRS tests, not immigration labels.

2. Incorrectly Calculating Days in the U.S.

Many people miscalculate the Substantial Presence Test by counting days incorrectly. Even small errors can change your tax classification, leading to incorrect filing as either a resident or non resident.

3. Filing the Wrong Tax Form

NRAs must typically file Form 1040-NR, but some individuals mistakenly file Form 1040, which is meant for residents. This can delay refunds or trigger IRS corrections.

4. Ignoring Tax Withholding Rules

Some NRAs assume that no tax is due if money is already received. However, many types of U.S. income are subject to withholding, and failing to account for this can result in underpayment issues.

5. Missing Tax Treaty Benefits

Many countries have tax treaties with the U.S. that reduce tax rates or provide exemptions. Not claiming these benefits means paying more tax than necessary.

Tax Treaties and Special Rules for Non Resident Aliens

Tax treaties play an important role in reducing or eliminating double taxation for Non Resident Aliens (NRAs). These agreements are made between the United States and other countries to ensure that individuals do not pay tax twice on the same income. The rules are administered under the framework of the Internal Revenue Service, which also provides guidance on how treaty benefits can be claimed.

1. What Are Tax Treaties?

Tax treaties are formal agreements between two countries that define how income should be taxed when a person earns money in both jurisdictions. These treaties often specify reduced tax rates or exemptions for certain types of income such as wages, scholarships, pensions, and royalties.

2. How Treaties Benefit Non Resident Aliens

For NRAs, tax treaties can significantly lower the amount of tax withheld on U.S.-sourced income. In some cases, certain income may be completely exempt from U.S. taxation if the conditions of the treaty are met. This helps individuals keep more of their earnings and avoid being taxed twice on the same income in both countries.

3. Eligibility Requirements

Not everyone automatically qualifies for treaty benefits. NRAs must usually be residents of a country that has a tax treaty with the U.S. and must properly declare their eligibility when filing taxes. This often involves submitting specific forms along with their tax return.

4. Common Treaty-Included Income Types

- Employment income

- Student scholarships and grants

- Pension income

- Investment income

Understanding tax treaties is essential for NRAs because they can significantly reduce tax liability and improve financial efficiency when earning income in the United States.

Reporting and Compliance Rules for Non Resident Aliens

Non Resident Aliens (NRAs) are required to follow specific reporting and compliance rules when earning income from the United States. These rules ensure that all taxable income is properly declared and that the correct amount of tax is paid. The system is regulated by the Internal Revenue Service, which enforces strict guidelines for foreign taxpayers.

1. Required Tax Forms

The primary form used by NRAs is Form 1040-NR, which is specifically designed for non resident taxpayers. This form is used to report U.S.-sourced income, claim treaty benefits, and calculate final tax liability. In some cases, additional forms may be required depending on the type of income earned.

2. Employer and Payer Reporting

Employers and financial institutions in the U.S. are also required to report payments made to NRAs. This includes wages, dividends, interest, and other taxable income. Proper documentation ensures that withholding taxes are correctly applied and reported.

3. Record-Keeping Requirements

NRAs should maintain accurate records of income, tax withheld, and supporting documents such as visa details and travel history. These records are important in case of audits or when claiming tax refunds or treaty benefits.

4. Filing Deadlines and Extensions

Tax filing deadlines for NRAs are generally similar to those for U.S. residents, but extensions may be available depending on individual circumstances. Filing on time is essential to avoid penalties and interest charges.

5. Penalties for Non-Compliance

Failure to report income correctly or file required forms can result in penalties, delays in refunds, or legal consequences.

Real-Life Examples of Non Resident Alien Status

Understanding Non Resident Alien (NRA) rules becomes much easier when we look at real-life situations. These examples show how different individuals can fall under NRA classification depending on their residency status, income source, and time spent in the United States. The rules are determined by the U.S. tax system administered by the Internal Revenue Service.

1. International Student Example

A student from Pakistan studying in the United States on an F1 visa is often treated as a Non Resident Alien, especially during the first five calendar years. Even if the student earns part-time income on campus, that income is taxed only as U.S.-sourced income. The student is not required to report global income in most cases, which simplifies tax reporting.

2. Foreign Freelancer Example

A freelance web designer living in India who works for clients in the United States is also considered an NRA. Even though they never physically enter the U.S., their income from U.S. clients may still be subject to U.S. tax rules depending on how the payment is classified and sourced.

3. Temporary Worker Example

A software engineer from another country working in the U.S. on a short-term H1B visa may be classified as an NRA if they do not meet the Substantial Presence Test. Their salary is taxed only on income earned within the U.S.

4. Investor Example

A foreign investor earning dividends from U.S. stocks or rental income from U.S. property is also considered a Non Resident Alien for tax purposes. Their income is taxed separately under withholding rules.

Frequently Asked Questions (FAQs) about Non Resident Alien

Understanding Non Resident Alien (NRA) status often raises many questions, especially for students, workers, and foreign investors dealing with U.S. tax rules. Below are some commonly asked questions with clear answers based on guidelines from the Internal Revenue Service.

1. What does Non Resident Alien mean in simple words?

A Non Resident Alien is a person who is not a U.S. citizen and does not meet the tax residency tests. They are taxed only on income earned from U.S. sources.

2. Do Non Resident Aliens pay tax on foreign income?

No. NRAs are generally only taxed on income connected to the United States. Foreign income earned outside the U.S. is usually not taxed by the U.S.

3. Which tax form do Non Resident Aliens use?

Most NRAs must file Form 1040-NR, which is specifically designed for non resident taxpayers.

4. How do I know if I am a Non Resident Alien or Resident Alien?

Your status depends on the Green Card Test and Substantial Presence Test. If you fail both, you are considered an NRA.

5. Can Non Resident Aliens get tax refunds?

Yes, if too much tax was withheld from their U.S. income, they may be eligible for a refund after filing their tax return.

6. Are Non Resident Aliens eligible for tax benefits?

Some benefits may be available through tax treaties, but most standard deductions and credits are limited.

Conclusion

Understanding the Non Resident Alien classification is essential for anyone earning income from the United States while not being a citizen or tax resident.

This status directly affects how income is taxed, what forms must be filed, and what benefits or limitations apply under U.S. tax law. Whether you are a student, worker, freelancer, or investor, your tax obligations depend on whether you meet the residency tests or fall under NRA rules.

Throughout this guide, we explored how the classification is determined using the Green Card Test and Substantial Presence Test, how different types of income are taxed, and what filing requirements must be followed. We also looked at key differences between resident and non resident aliens, along with common mistakes and compliance rules.

Hi, I’m Jordan Sylar, and I write here at Pickupsy.com. I’m a Senior Research Analyst with a passion for helping people discover insights, learn new things, and achieve their goals.

I hold a Master’s degree from Yale University and a B.A. in Biblical and Theological Studies from Lee University.

{kind=link}